New Methods in Crisis Modeling (Proc. FISS MASR, 2005)

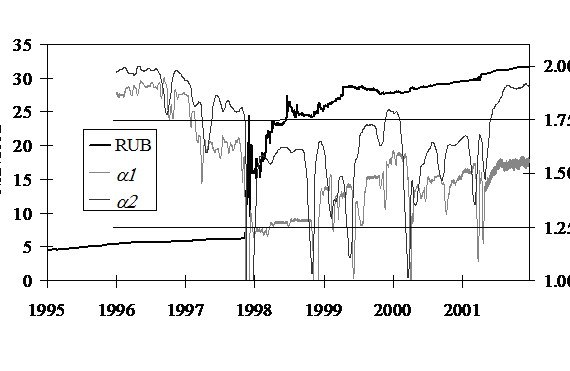

Results of fractal analysis of daily exchange rate fluctuations of floating currencies for a 10-year period are presented. It is shown that monetary crashes are usually preceded by prolonged periods of abnormal fractal exponent. Regression relations between duration and magnitude of currency crises and the degree of distortion of monofractal patterns of exchange rate dynamics